Y’s Tips Channel

このチャンネルは、日本に住む外国人のために日本の暮らしに必要な情報を英語で提供します。

#27 Tax benefit of defined contribution (確定拠出年金の税制メリット)

Today I’d like to talk about the tax benefit of defined contribution.

今回は確定拠出年金の税制メリットについてお話します。

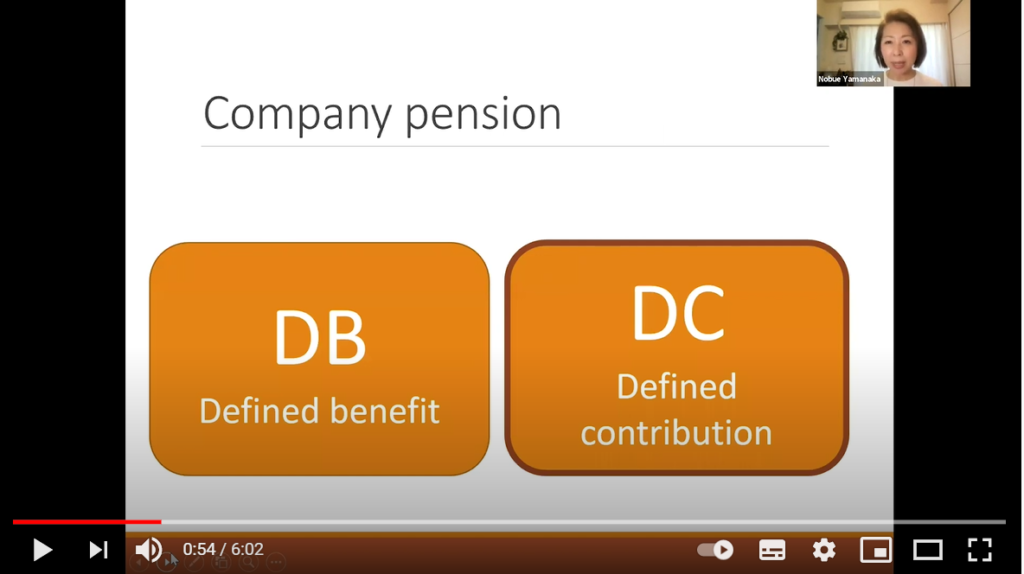

In Japan many companies have company pensions. There are two types of them. One is called DB, another one is called DC. DB is an abbreviation for defined benefit. If your company provides you DB you don’t have to worry about too much. Because your company guarantees you the amount you can receive in your future. On the other hand, if your company provides you DC, which is an abbreviation for defined contribution, you have to be more careful. Because your company guarantees you only the contribution, the amount you can receive in your future depends on your investment. You have to take care of your DC by yourself.

日本では多くの会社に企業年金があります。企業年金に2つのタイプがあり、ひとつはDB、もうひとつはDCと呼ばれています。DBとは確定給付企業年金のことです。もしあなたの会社がDBであれば、あまり心配する必要はありません。なぜならばDBは将来あなたが受け取る金額を会社が保証しているからです。一方会社がDC(企業型確定拠出年金)を導入しているのであれば、注意が必要です。なぜならば会社が保証するのは掛金の拠出のみで、将来の受取る金額はあなたの運用次第、あなた自身で管理しなければならないのがDCだからです。

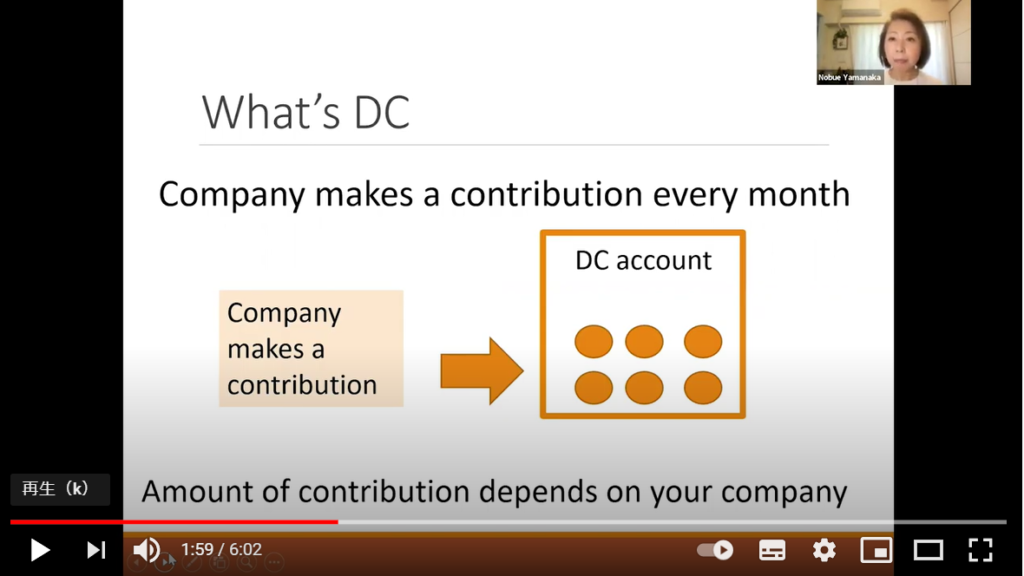

DC is just like a bank account. Your company put your contribution into your account. Here contribution means premiums, some amount of money you can receive from your company. The amount of contribution depends on your company.

DC というのは口座のようなものです。会社はあなたの口座にcontribution を入金します。ここでは、掛金という意味で、会社があなたの口座に積立てくれるお金です。この掛金は会社ごとに異なります。

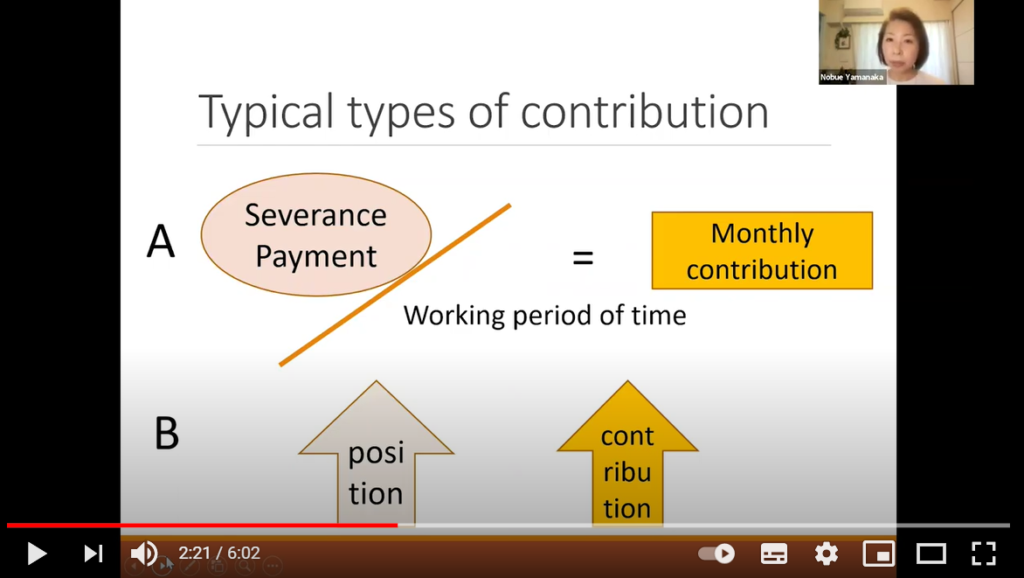

I would like to introduce you typical types of contribution. The type A, your company assumes a severance payment and divided by working period of time. In this means your contribution is just like a divided retirement payment in advance. The type B, your contribution increases if your position gets higher. In this case your contribution is just like a promotional allowance. There are different types of contributions so if you have a DC, please go ahead to ask your company.

典型的な掛金の拠出についてお伝えします。タイプAは、想定される退職金を勤続年数で割ったものです。こちらは、退職金の前払いとしての掛金です。タイプBは、役職に応じて掛金が変わるものです。ただし掛金についてはいろいろな種類がありますので、会社がDCを導入しているという方は会社にお尋ねください。

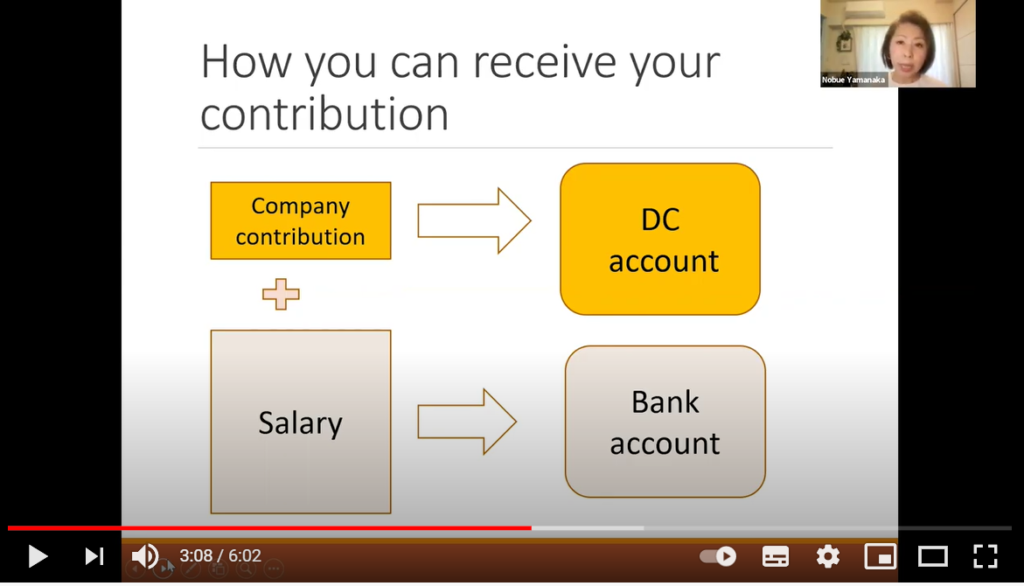

The most of the time your contribution is paid when your salary is paid. Your salary goes to your bank account. Your company contribution goes to your DC account. Those are looks almost the same but there is a big difference between two.

通常会社からの掛金は、給与の支払い時に支払われます。給与は銀行口座に振り込まれますが、会社からの掛金は確定拠出年金の口座に振り込まれます。この二つはよく似ていますが、とても大きな違いがあります。

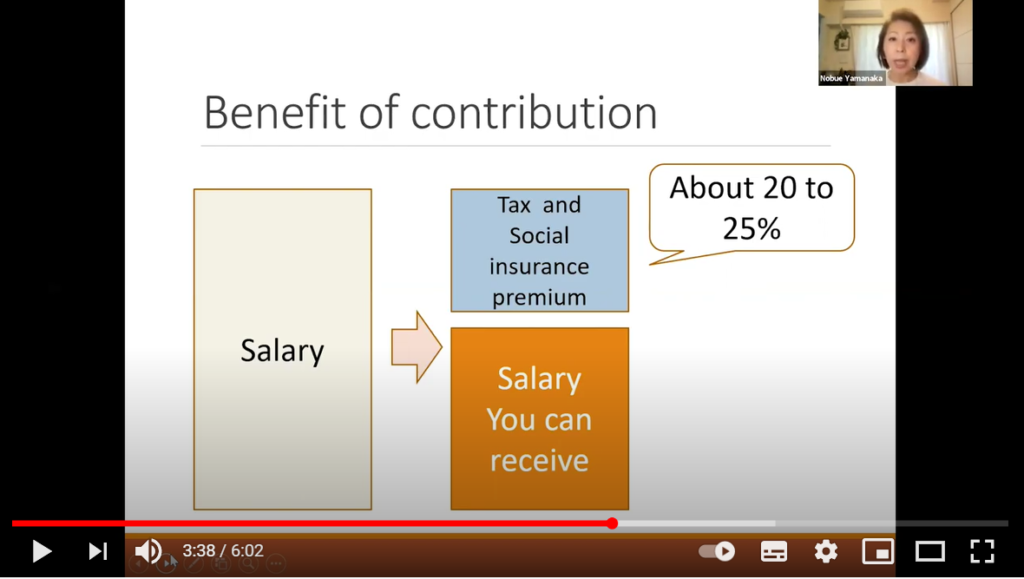

For example when you receive the salary you can’t receive all the money. Because you have to pay your income tax and social insurance premiums. That’s why you can receive only the remaining. Usually the tax and social insurance premiums are about 20 to 25 percent of your salary which is a quite big amount of money.

例えば給与を受け取る時、全額は受け取ることができません。なぜならば、所得税や社会保険料を支払わなければならないからです。受け取れるのは、それらを差し引いた後の金額です。通常税金と社会保険料は給与の20~25%です。結構な金額となります。

However, if you receive your company contribution you can receive all the money. There is no deduction. You don’t have to pay any income tax or social insurance premiums from the contribution. You can invest all the money for your future. This is the biggest tax benefit for defined contribution.

しかし、確定拠出年金の掛金は全額受け取ることができます。なにも差し引かれません。税金も社会保険料も確定拠出年金の掛金にはかからないのです。そのため掛金の全額を将来のために投資することができます。これが確定拠出年金の最も大きな税制メリットです。

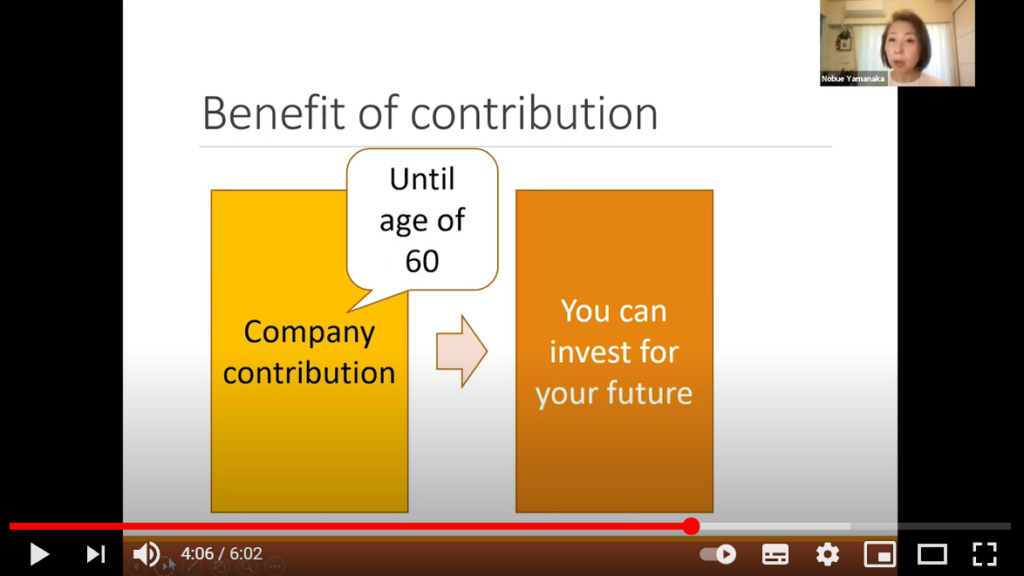

Once you receive contribution, you will make an investment. The contribution will be continued until age of 60, but you can continue the investment until age of 70.

掛金を受け取ったら、そのお金を投資に回します。掛金の拠出は60歳までですが、運用は70歳まで継続することができます。

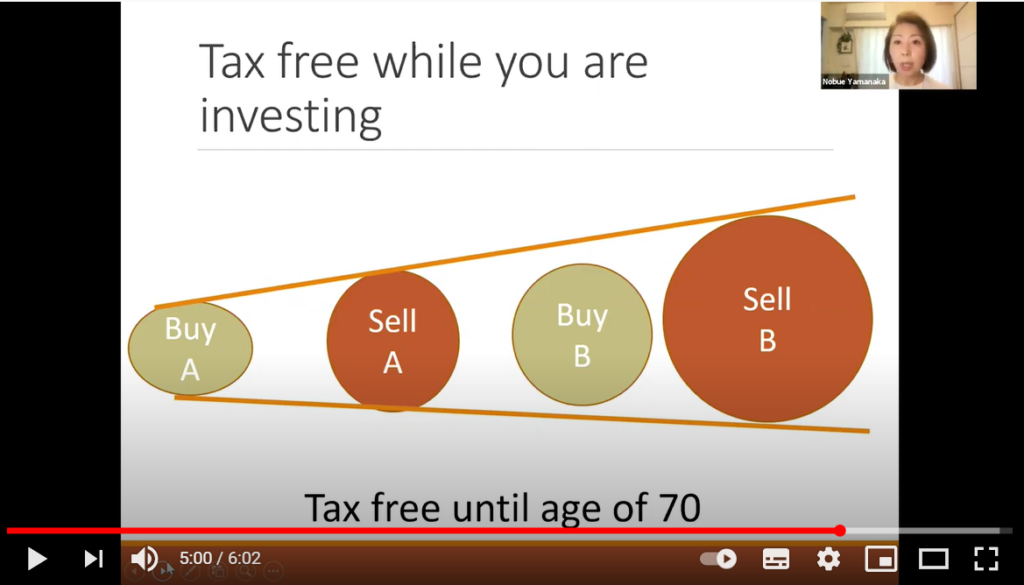

There is another tax benefit. Within DC account, if you make a profit you don’t have to pay any income tax. Usually if you make a profit from the investment, you have to pay over 20 percent of income tax. However within DC account, just like a NISA, you don’t have to pay any income tax. So you can enjoy the tax free until age of 70 as long as you continue the investment. This is the second tax benefit for defined contribution.

もうひとつ税金のメリットがあります。確定拠出年金の口座のなかで得た利益には税金がかかりません。通常投資で得た利益には20%を超えるぜ金がかかりますが、DCの口座の中で運用すると、ちょうどNISAのように、運用益が非課税になるのです。そのためDCにおいては、運用を続ける限り最長70歳まで運用益非課税で投資をすることができます。これが確定拠出年金の二つ目のメリットです。