Y’s Tips Channel

このチャンネルは、日本に住む外国人のために日本の暮らしに必要な情報を英語で提供します。

#29 HOW TO START AND HOW TO FINISH YOUR DEFINED CONTRIBUTION

確定拠出年金の始め方と終わり方

Today I’d like to talk about how to start and how to finish your Defined Contribution. Defined Contribution is especially designed for your retirement, you can develop your asset with tax benefit.

今回は確定拠出年金の始め方と終わり方についてお話します。確定拠出年金は税制優遇を受けながら老後の資産形成ができる仕組みです。

Let me give you a quick review what Defined Contribution is. From now on, let me call it bDC instead. DC is just like a bank account, you can save your money for your retirement. In this case your money is called contribution. Then in your DC account you can purchase some kind of financial products to develop your asset. You can continue your investment until your retirement. Besides that you can enjoy tax benefit. For example, all your contributions are income tax deductible. Your investment returns are reinvested tax-free. Also you can receive your money once you retire with tax benefit.

まず簡単な復習をしましょう。今後は確定拠出年金のことをDCを呼ばせていただきます。DCは銀行口座のように老後のためにお金を貯めておく場所です。この際あなたのお金を「掛金の拠出」と呼びます。DCでは拠出した掛金で金融商品を購入し運用をします。運用は老後資金として継続されます。これに加え、掛金は全額所得控除となりますし、運用益は非課税で複利運用されます。

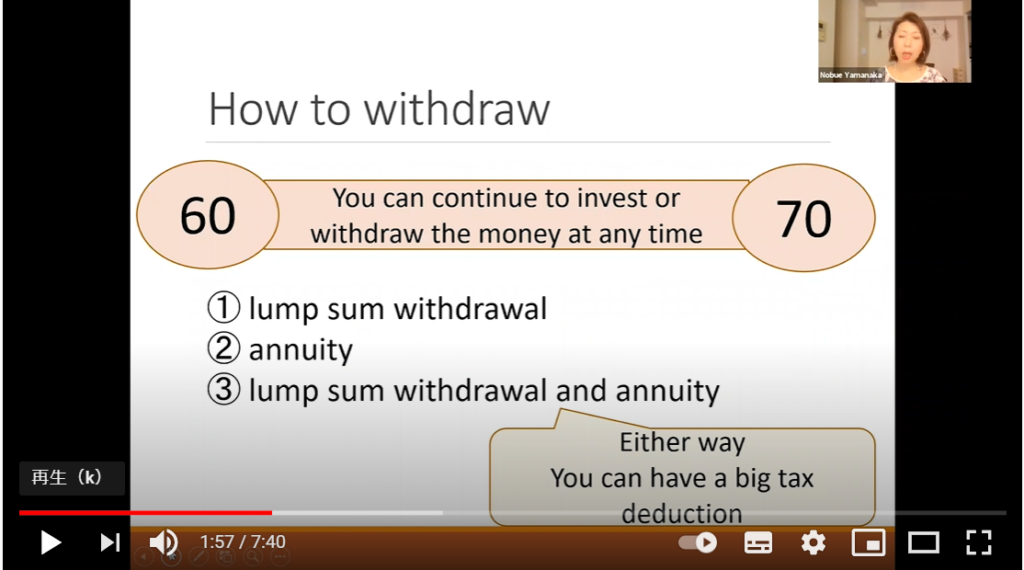

When you become age of 60 you can receive your money or you can continue your investment until age of 70. During this 10 years you can decide when you withdraw your money at any time. There are three ways to withdraw. Lump sum withdrawal, annuity and mix of the lump sum withdrawal and annuity. Either way you can have a big tax deduction. Those are good things about Defined Contribution.

60歳になるとお金を引き出すこともできますし、70歳まで運用を継続することもできます。この10年間のうち、好きなタイミングでお金の引き出しができます。受取時は一括、分割、併用の3つのパターンから受取方を選ぶことができます。いずれの受取方でも税控除が受けられます。これらがDCの良いところです。

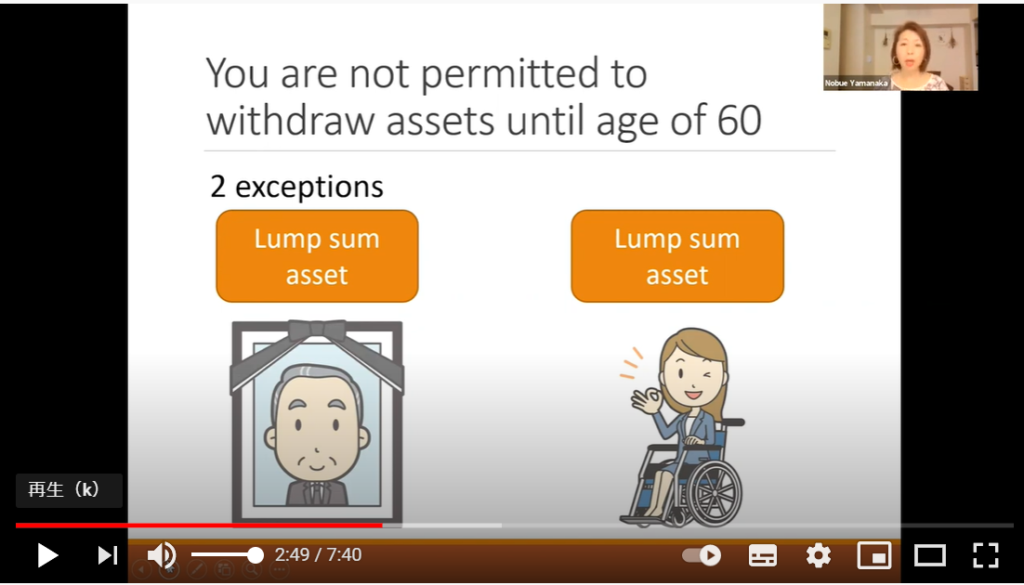

However you have to understand you are not permitted to withdraw asset until age of 60, which is strictly set by the law. There are only two exceptions you can withdraw your money before age of 60.If you die your family can receive your money as a death benefit or if you become disabled you can withdraw your money.

しかしながら、60歳までは資金の引き出しができないことは理解しておくべきでしょう。これは法律により定められています。

60歳になる前に資金の引き出しができるケースは2つあり、加入期間中に死亡した時は家族が死亡給付金を受取ますし、障害を負った時は障害給付金を受けられます。

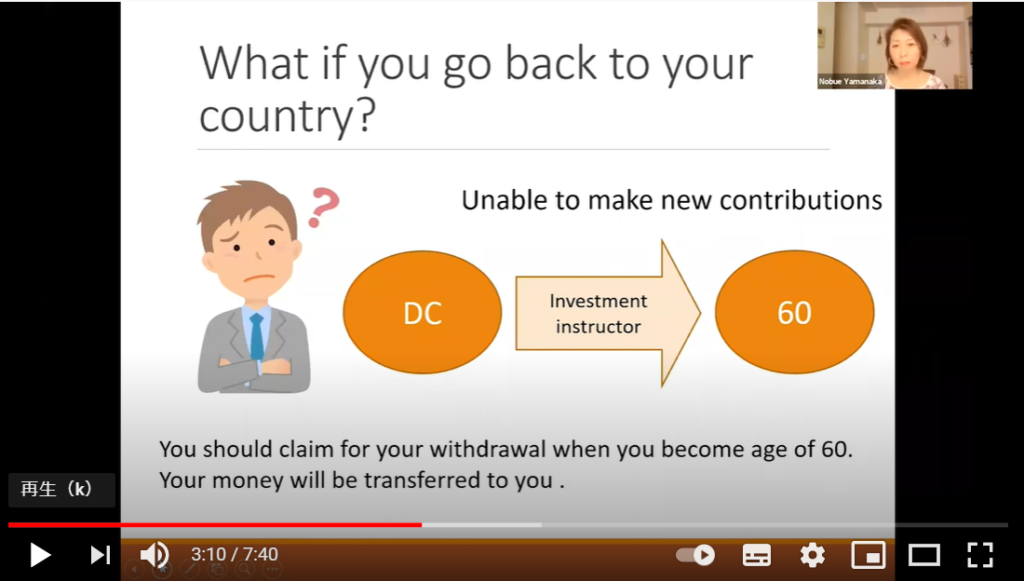

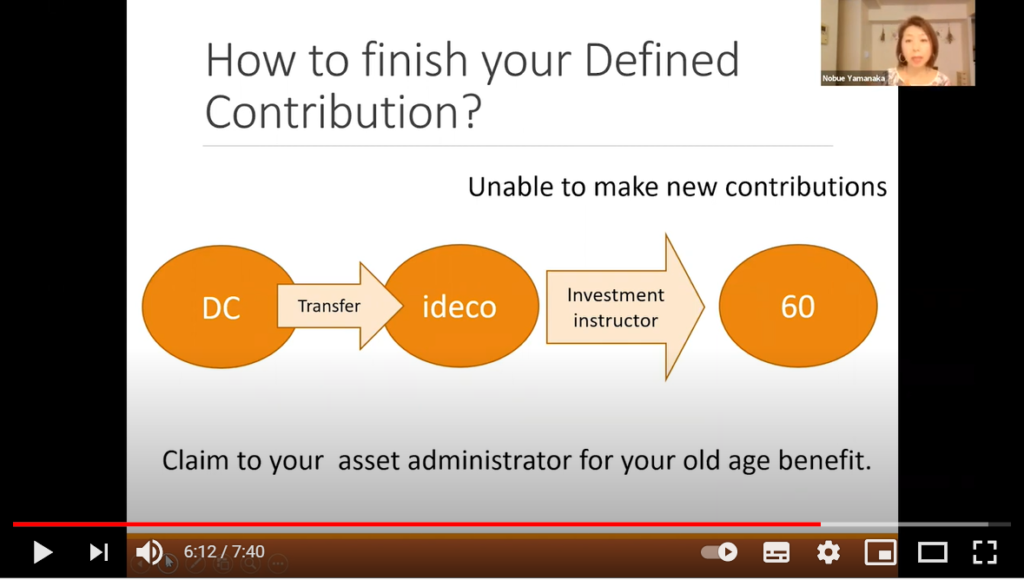

As a foreigner you may think what happen if you go back to your country. This law applies for foreigners too. So even though you are not in japan you have to keep your DC account in Japan. Of course you are not in japan you cannot make new contributions. So just keep your account as an investment instructor then once you become age of 60 you claim for your old age benefit.

外国籍の方は、帰国したらどうなるのだろうと思うでしょう。しかしこの法律は外国籍の方にも適用されます。そのためもし帰国されても、日本に口座を置いておく必要があります。当然新しい掛金の拠出はできませんので、運用指図者として口座を保有したままにして60歳になったら老齢給付を請求します。

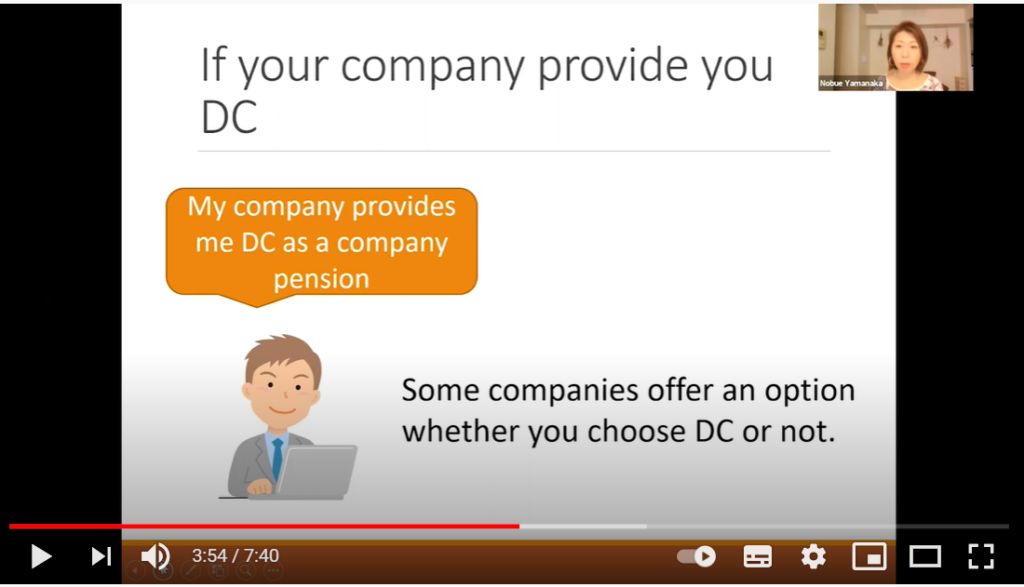

In fact many foreigners have dc account, because many companies provide them dc as a company pension systems. In most of the time, you have no choice to join the DC program. However some companies offer an option whether you choose DC or not. In that case you can say no if you don’t want to.

実際、多くの外国人の方がDC口座を利用しています。なぜならば、多くの会社で企業年金としてDCを利用しており、多くの場合その会社の従業員はすべて加入しなければならないからです。しかし、会社によってはDCに参加するかどうかを選べるところもあり、その場合もし希望しなければ断ることもできます。

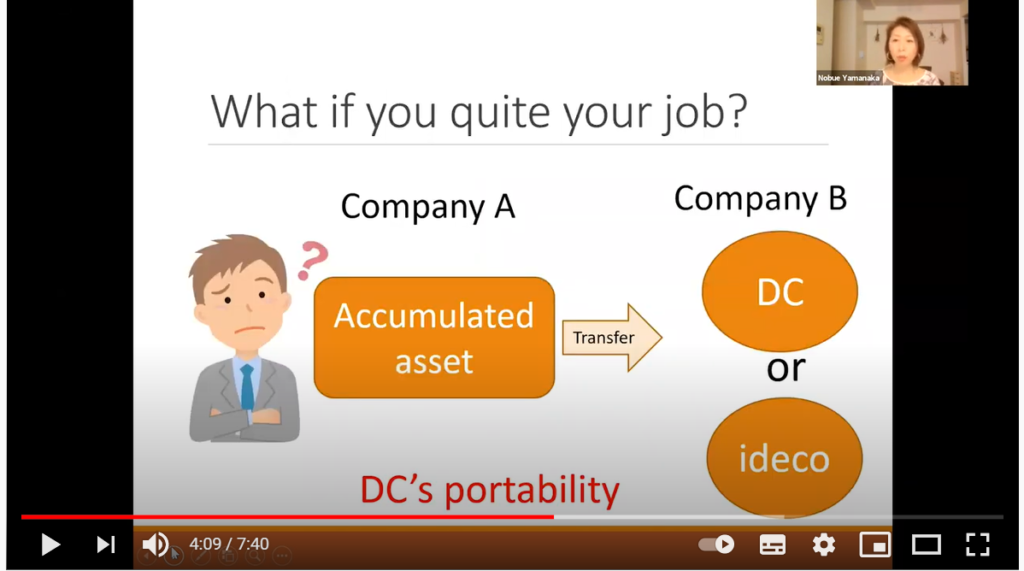

Anyway once you open your dc account, you have to keep it until your retirement. Then what happen if you quit your job, since DC is one of your company’s pension system if you quit your job you have to do something. There are two options. If your new company have DC program, in that case you can transfer your accumulated assets into your new DC account or you can open ideco account by yourself and you can transfer your accumulated asset into your ideco account. Either way you can continue your investment with tax benefit. This is called DC’s portability.

とにかくいったんDC口座を開くと、リタイアするまで続けなければなりません。では、会社を辞めたらどうなるでしょうか?会社の企業年金として加入するDCは、会社を辞め時はなにか手続きをしなければなりません。その場合2つの選択肢があります。もし新しい会社に企業型DCがある場合は、その会社のDCに資産を持ち運びます。あるいは、自分でiDeCo口座を開設しそこに資産を持ち運ぶこともできます。いずれにせよ、税制優遇を受けながら資産形成を継続することができます。これを確定拠出年金のポータビリティと呼びます。

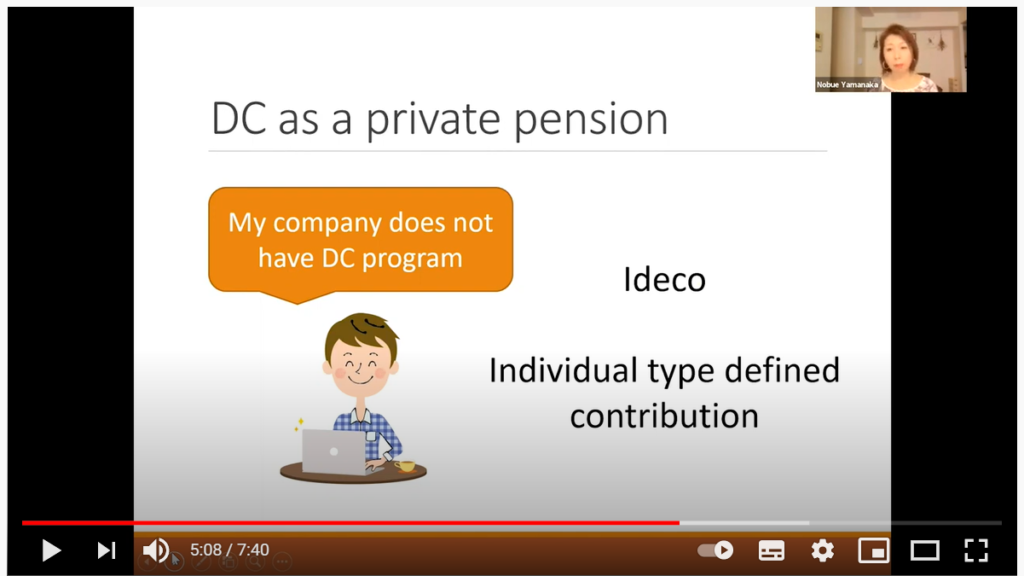

ideco is another type of defined contribution which is a private pension. People who don’t have a company pension can use ideco. ideco has a tax benefit too just like DC.

iDeCoは、もうひとつの確定拠出年金でこちらは私的年金です。お勤め先に企業型DCがない方などが利用します。iDeCoも企業型DCと同様に税制優遇があります。

If you want to start ideco, at first you have to open your ideco account at the asset administrator . Asset administrator is a financial institutions such as banks, security companies, insurance companies and so on. Those company takes care of your ideco account. Since you may have a lot of paperwork you may want to use a helpful asset administrator. As long as I know SBI security company and DAIWA security company have an English page on their website. So those two can be your recommendation.

iDeCoを始めるには運営管理機関に口座を開設する必要があります。運営管理機関とは窓口金融機関のことで銀行、証券会社、保険会社などがなります。運営管理機関がiDeCo口座に関する情報を提供します。いくつか書類の手続きがあるかも知れないので、便利が運営管理機関を選ぶ必要があります。私が知る限り、SBI証券と大和証券は英語のページがありますので、もしかしたらこの2社はお勧めかも知れません。

Let me conclude today’s topic how to finish your Defined Contribution. If you are in Japan at the age of 60 and you use DC as a company pension you claim for your old age benefit to your company. And your company helps you what to do. If you’re in Japan at the age of 60 you use ideco , you claim for your old age benefit to your asset administrator. If you are not in Japan you have ideco you claim for your old age benefit to asset administrator. That’s something I want you to understand about Defined Contribution.

さあ、今回のトピックスについてまとめます。もしあなたが60歳の時に日本にいて、かつ企業型DCをしている時は、会社に老齢給付の申請をします。会社が何をすべきか教えてくれるでしょう。

もし60歳の時日本にいて、iDeCoをしている場合、運営管理機関に老齢給付の申請を行います。もし日本にいない場合、運営管理機関に申請します。以上がみなさんに知っておいていただきたい確定拠出年金についてでした。

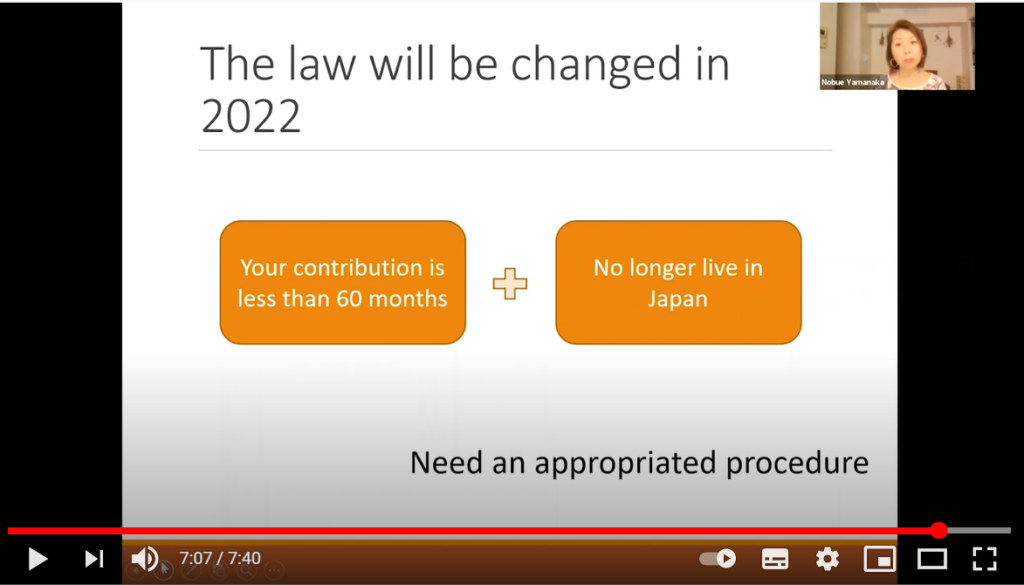

I have one more information. The law will be changed in 2022. The new law say if your contribution is less than 60 months and at the same time you don’t live in Japan anymore you can withdraw your money as exception. We don’t know much about the law yet but it can be good news for somebody.

2022年に法律が変わり、加入期間が60ヶ月未満でかつ日本を離れる場合は脱退一時金が受けられるようになる予定です。詳細はまだ分かりませんが、これがプラスとなる方もいらっしゃるでしょう。