Y’s Tips Channel

このチャンネルは、日本に住む外国人のために日本の暮らしに必要な情報を英語で提供します。

#26 Check your severance pay system (退職金制度を確認しよう)

Today I’d like to talk about the necessity of checking your severance pay system.

今回は退職金制度を確認する必要性についてお話します。

In Japan most of the company sets a retirement age at 60 or 65. When you become at the age usually you can have a quite big amount of money0 as a severance payment. It’s very important to know how much you can have in advance in order to prepare your retirement.

日本では多くの会社が定年を60歳または65歳で定めています。あなたがその年齢に達すると、通常まとまった金額で退職金が支払われます。退職金がいくらなのかを事前に知ることは、ご自身の老後に備えるためにとても重要です。

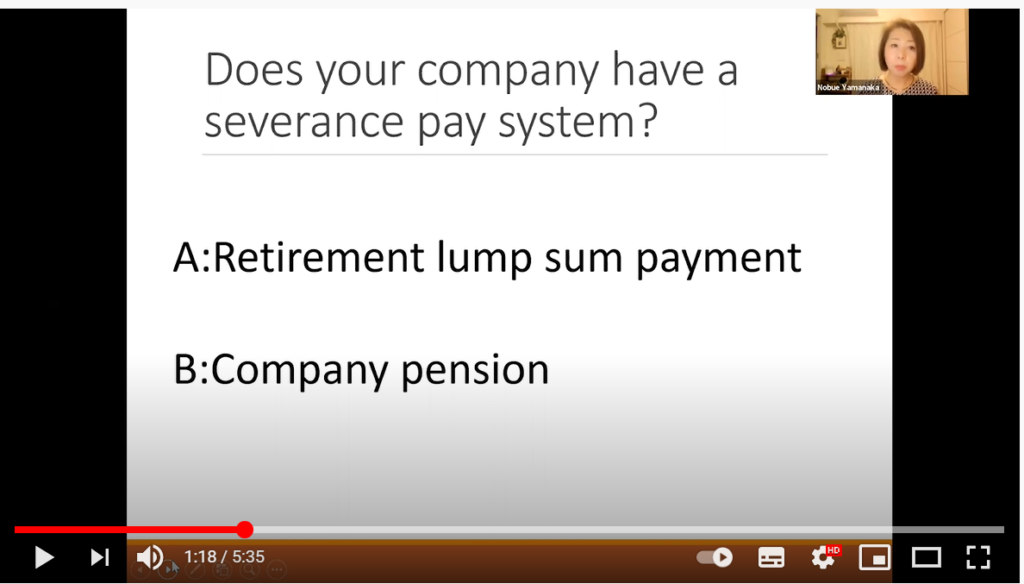

There are two types of severance payment. One is retirement lump sum payment, another one is company pension. The first one is paid at once, the second one is paid as an annuity for the certain period of your time.

退職金制度には二種類あります。退職一時金と企業年金です。退職一時金は一括で支払われますが、企業年金は年金として一定期間支払われます。

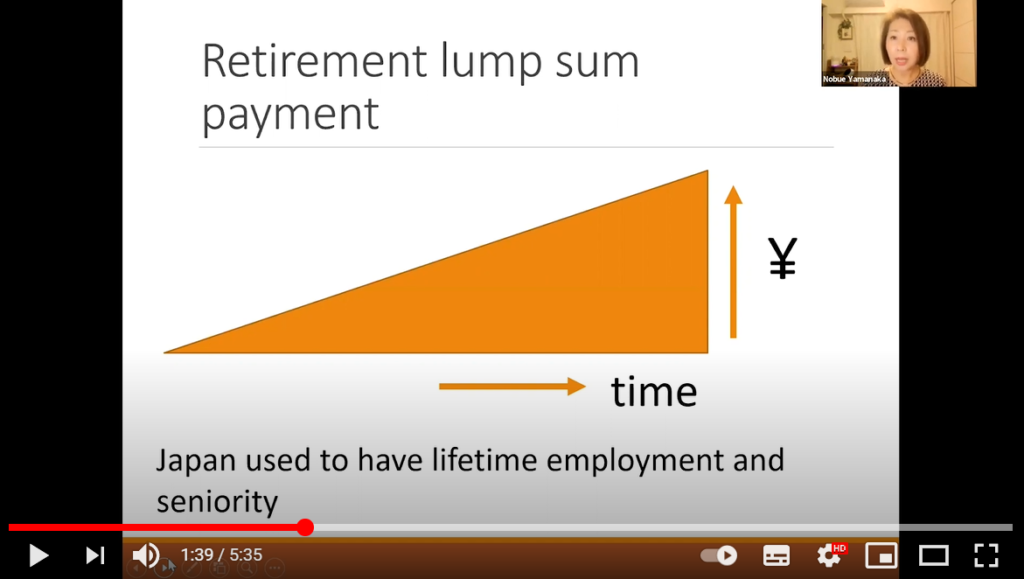

With retirement lump sum payment the amount gets bigger as the period of your time for the working become longer. Since Japan used to have or still have lifetime employment and seniority the amount usually depends on how long you have worked for the company.

退職一時金は、勤続年数が長くなるほど金額が大きくなることが通常です。これは日本がかつて、あるいは今でも年功序列、終身雇用である名残のためです。

However the amount you can have totally depends on your company. Since it’s not duty for the all company provides you the retirement payment, so some company have good system some companies don’t. Even some companies don’t have those payment system at all.

退職金の額については、完全に会社ごとによって異なります。なぜなら、退職金を支払うことは会社の義務ではないので、会社によってはとても良い制度があるところもあるし、そうではないところもあります。また退職金制度を待ったうないところもあります。

If you have one, you are lucky. Because when the income tax for the retirement payment is calculated you can use much more tax deduction which means you can receive your money very efficiently.

もしあなたの会社に退職金制度があれば、とてもラッキーです。なぜならば退職一時金の税金では、多くの控除が利用できるので、とても有利にお金が受け取れるからです。

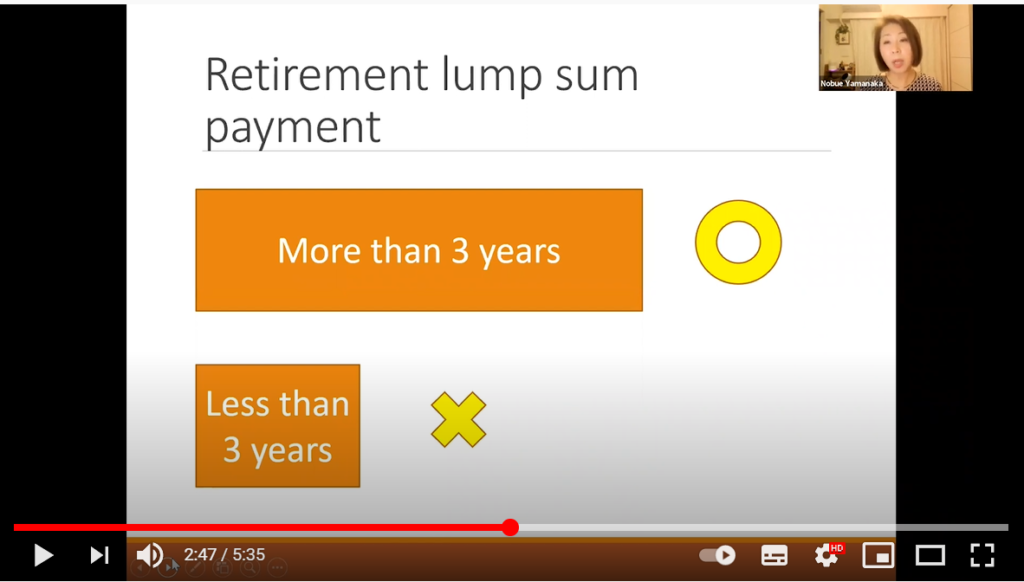

Retirement lump sum payment is not only paid after your retirement age but also it is paid when you quit your job before 60. For example, usually if you work for the company more than three years, you can have something. But less than three years you can’t have anything.

退職一時金は定年の時だけ支払われるわけではなく、定年前で会社を辞めた時でも支払われます。多くの会社では3年以上の勤続であれば何かしら退職金がでることが多く、3年未満はなにも出ないのが通常です。

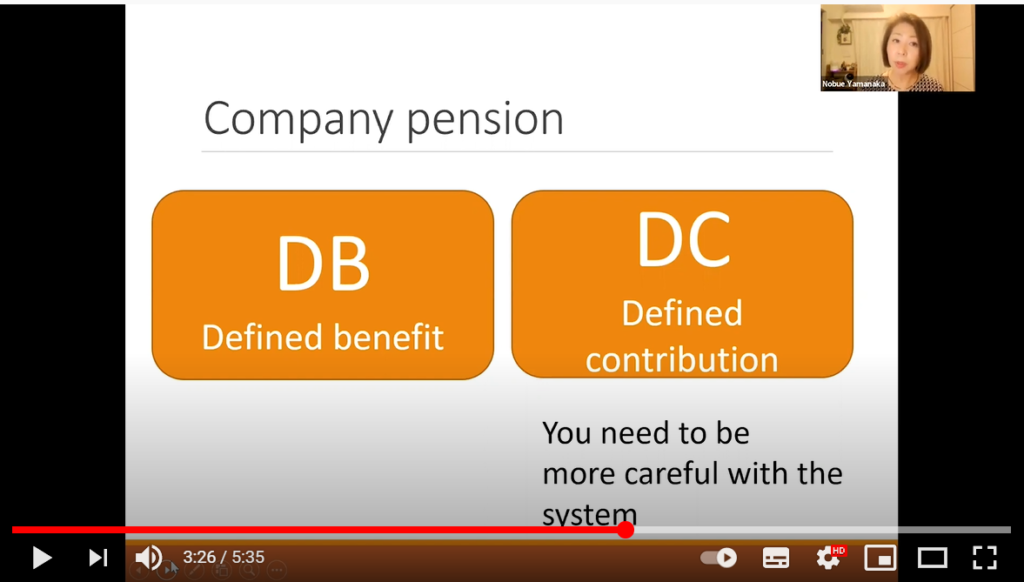

Let’s move on to the company pension. There are two types of company pension, one is called DB another one is called DC. DB is the abbreviation for the defined benefit if your company provides you DB, please go ahead to ask your company how much you can have in your future. Because with DB your company guarantee you the amount. On the other hand, DC is quite different from DB. DC is the abbreviation for defined contribution you need to be more careful with the system.

では、企業年金に移りましょう。企業年金にも2種類あり、ひとつはDBと呼ばれ、もうひとつはDCと呼ばれています。DBは確定給付年金です。もしあなたの会社がこの制度であれば、将来いくらになるのか確認しましょう。なぜならばDBは将来の支払い額を会社が保証するものだからです。一方DCはDBと全く違うものです。DCとは確定拠出年金のことで、この制度はもう少し注意深く確認する必要があります。

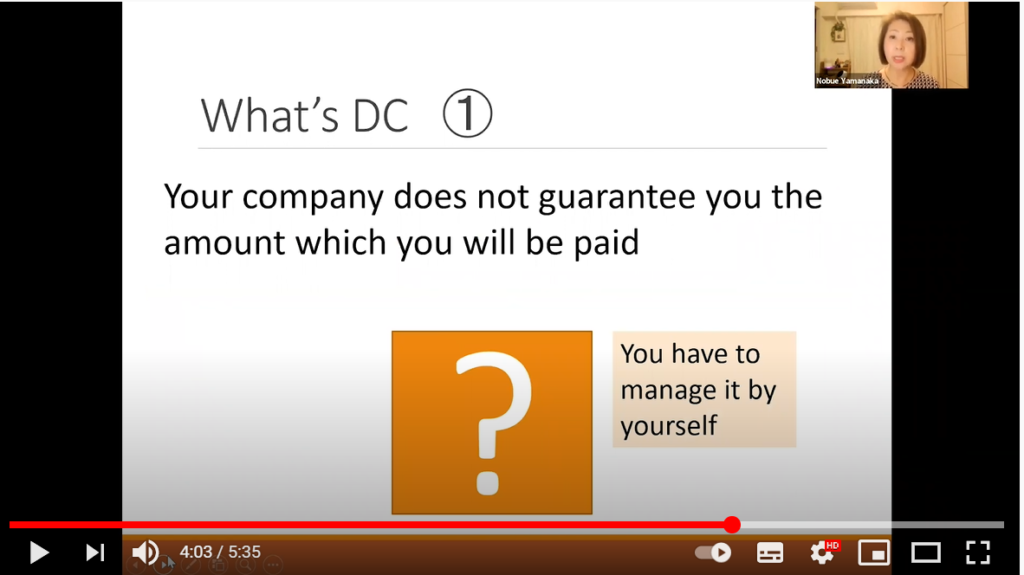

There are mainly three things you have to be more careful with. Number one with DC your company doesn’t guarantee you the amount which you will be paid. So you have to manage it by yourself.

DCについては主に3つの点で注意が必要です。まず最初に、DCは将来の支払い金額を会社が保証するものではないので、自分で管理する必要があります。

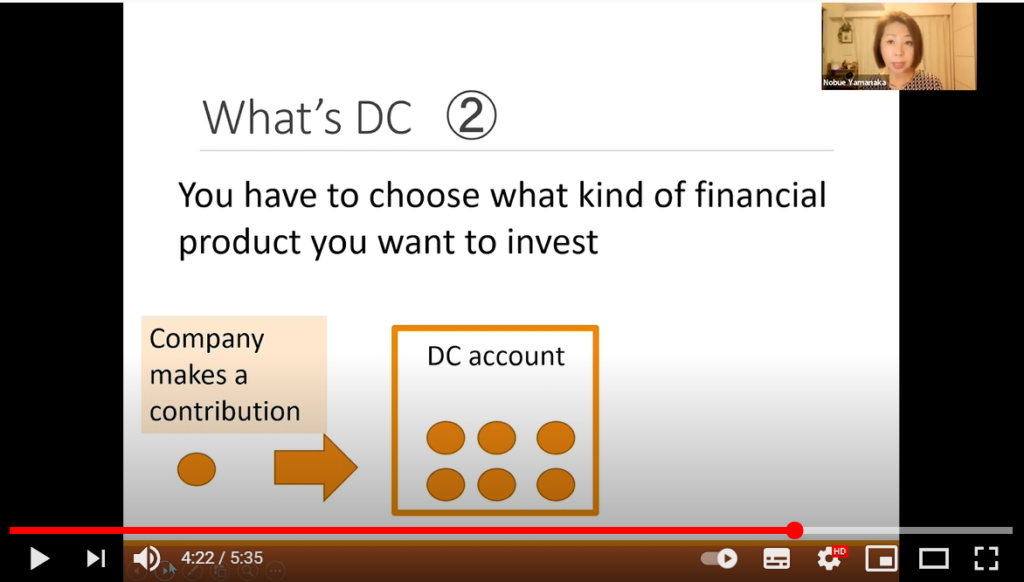

Number two, because DC is just like a money account, your company puts some amount of money as a contribution into your DC account. Then you have to choose what kind of financial product you want to invest, otherwise your money can’t grow at all.

2点目は、DCとは口座なので、会社はあなたの口座に掛金を拠出するだけです。そのお金をあなた自身が金融商品を選び運用していく必要があります。それをしなければあなたのお金は全く成長しません。

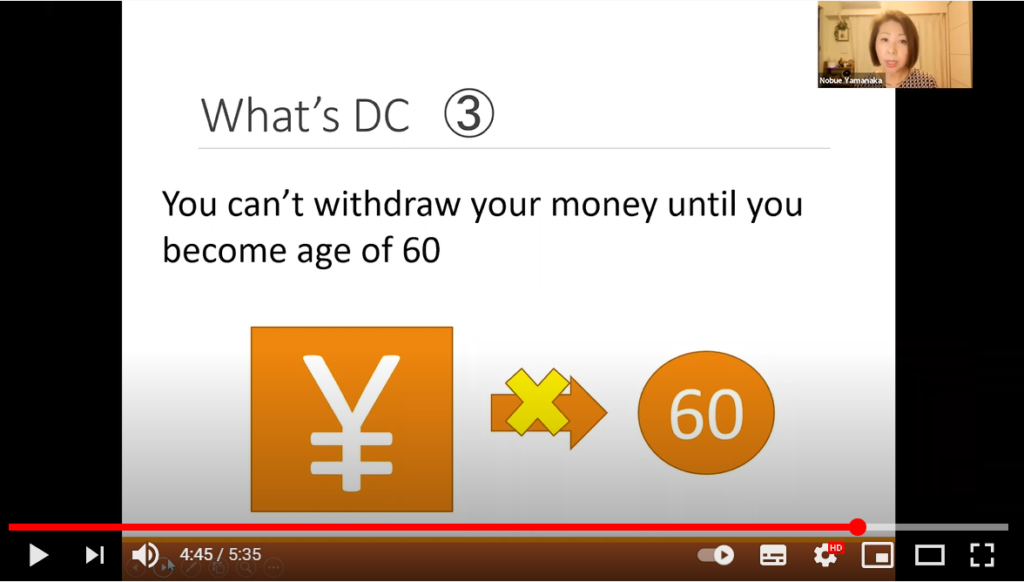

Number three under a Japanese law, you can’t withdraw your money until you become age of 60. Even though you go back to your country you can’t withdraw it. In fact DC is quite a good system when it comes to the taxation and asset formation, but it’s not good for everyone. I’d like to talk more about DC in my next video.

3点目は、日本の法律でDCのお金は60歳まで引き出しできないことになっていることです。もしあなたが自分の国に帰国したとしても引き出しができません。事実、DCは税金面や資産形成面でとても優れた制度なのですが、すべての人にとって良いとも限りません。DCに関しては次回の動画でもう少し詳しくお話します。