Y’s Tips Channel

このチャンネルは、日本に住む外国人のために日本の暮らしに必要な情報を英語で提供します。

#23 NISA Tax free program for investing(NISA について)

Today I’d like to talk more about deductions for reducing your income tax.

今回は所得税を引き下げる控除について、さらに詳しくお話します。

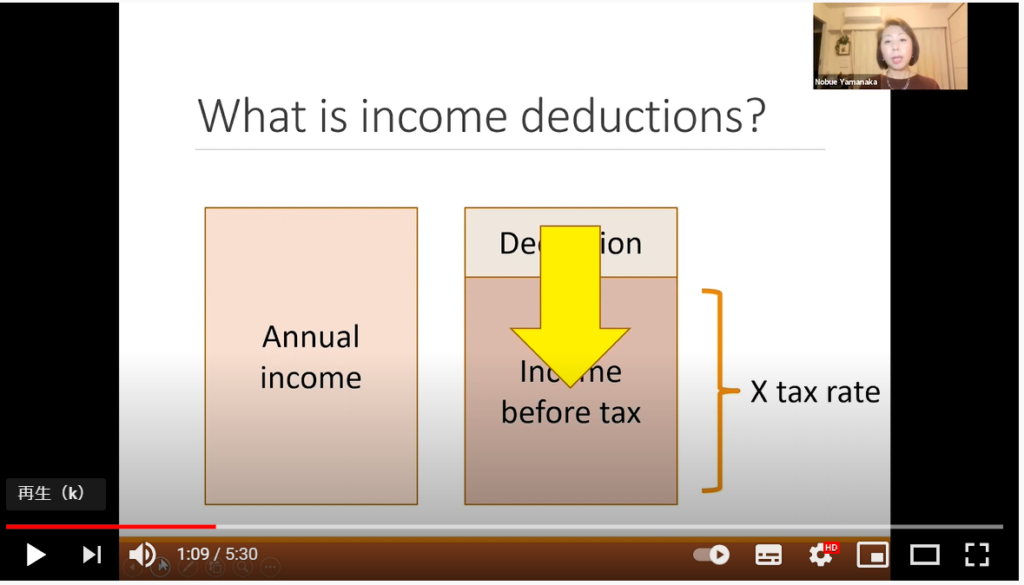

When your income tax is calculated you can deduct some amount of money from your annual income as expenses. If you can deduct more which means you can reduce your income before tax. As a result your income tax is decreased.

所得税の計算では、経費として認められる控除を年収から差し引くことができます。つまり控除を使えば課税所得が減り、結果として所得税を減らすことになります。

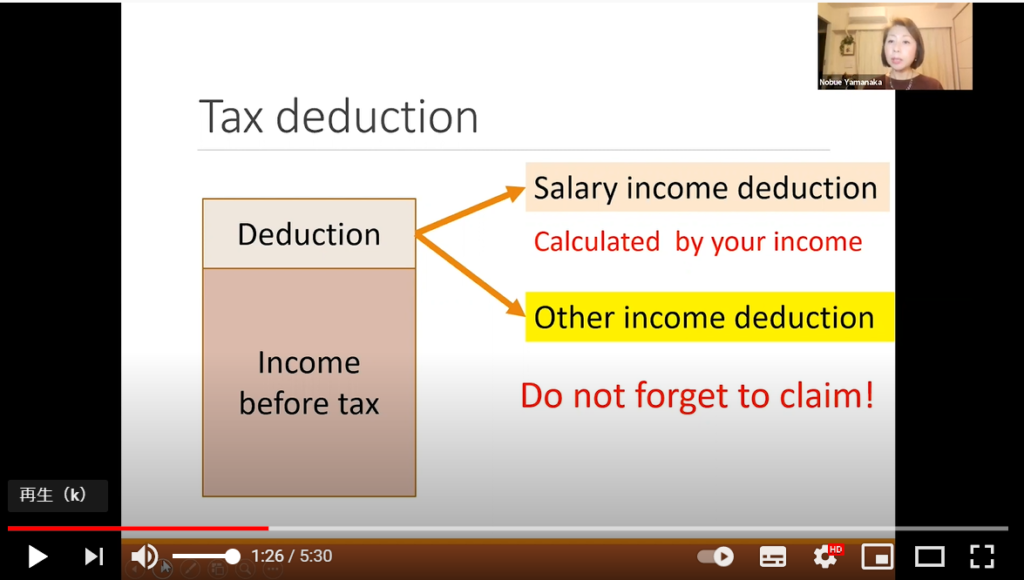

There are two types of tax deduction. One is salary income deduction another one is other income deduction. Salary income deduction is calculated by your income, which is fixed. This is calculated automatically. So you don’t have to do anything. However other income deduction is different depending on your situation. So you’d better to know what kind of deduction you can use. Unless you claim it you will not get any tax benefit.

控除には2種類あります。一つが給与所得控除、もうひとつがその他の所得控除です。給与所得控除は、年収により自動的に計算されるので、なにもする必要はありません。しかしその他の所得控除は個人の状況により異なるため、それぞれがどういう控除が使えるのかを知る必要があります。もし自分自身で申請しないと、税のメリットを受けることができません。

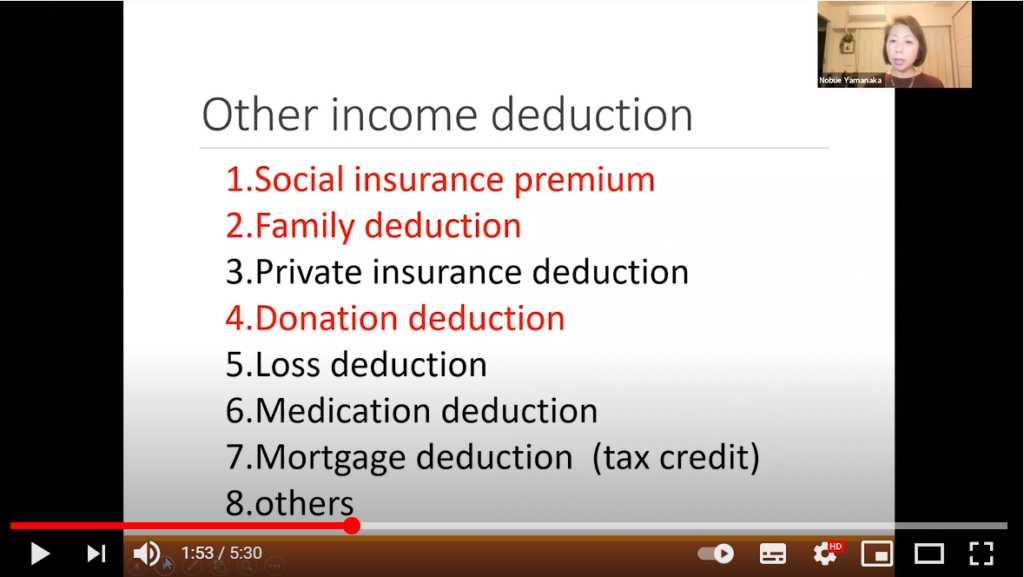

This is a list of other income deductions which I think are applied for many people. Number one, number two and number four are explained already in my previous video. So I’m going to tell you others.

こちらは私が多くの方に関係があると考えるその他の主な所得控除のリストです。No1,2,4はすでに以前の動画でお伝えしましたので、今回はその他についてお話します。

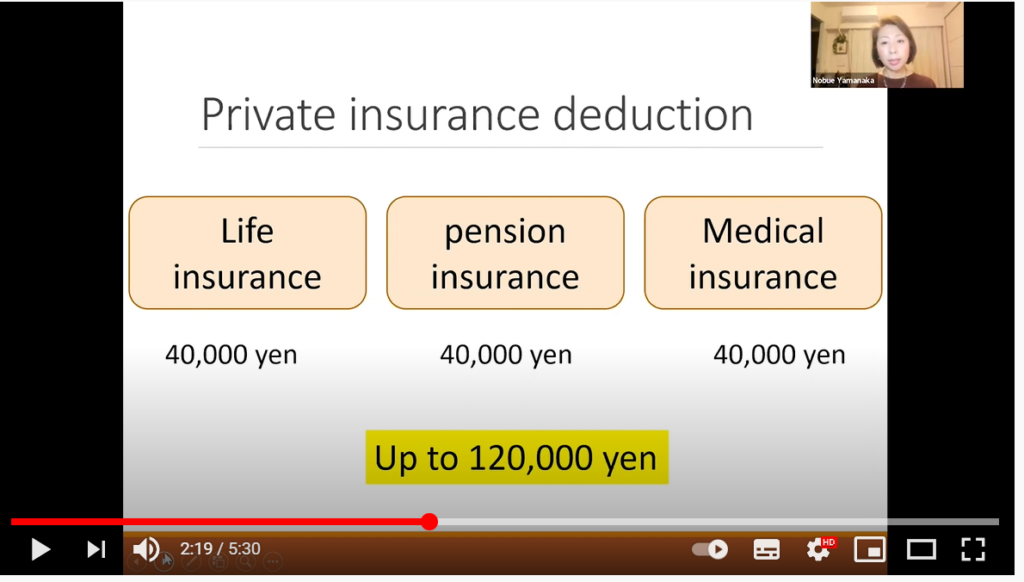

First of all you can use private insurance deduction, if you have a life insurance , pension insurance or medical insurance. For example, if you pay more than 80,000 yen as a premium for life insurance, you can deduct 40,000 yen as a private insurance deduction. The amount of the deduction is different according to how much is your premiums. The same goes to other two . You can deduct up to forty thousand yen for each insurance categories.

まず最初に、生命保険料控除です。もしあなたが生命保険、個人年金保険、医療保険への加入があれば、この控除を使えます。例えば生命保険料を年間8万円以上支払っている場合、4万円の控除ができます。控除額は、払った保険料の額によって異なります。これは他の2つにも当てはまり、それぞれ4万円を上限に控除が認められています。

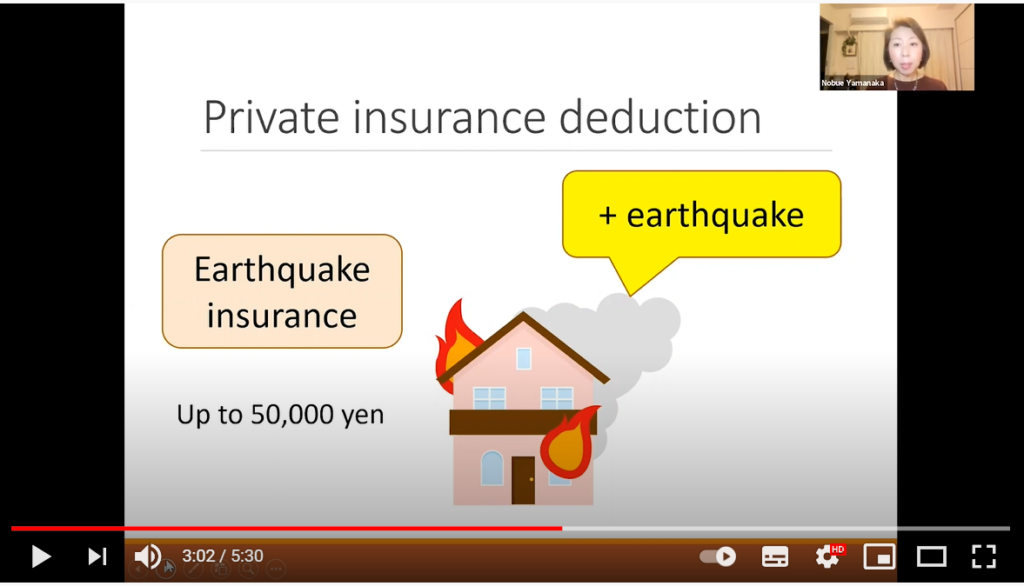

Also you can deduct up to 50,000 yen, as a earthquake insurance deduction. There is one thing many people misunderstand. Many people think if you have a fire insurance earthquake insurance is covered automatically. However this is not correct. Earthquake insurance is an option for fire insurance so if you want to have one, you have to ask for it.

また地震保険に入っている場合は5万円を上限に控除を受けることもできます。ただ多くの方が火災保険に入っていると自動的に地震保険に入っていると考えていますが、これは間違いです。地震保険は火災保険のオプションなので、希望する方はあらためて加入を申出しなければなりません。

Next one is loss deduction. In case of natural disaster or robbery you can claim some part of your loss as a deduction. It doesn’t cover everything, but it can be a big help.

自然災害や盗難にあった場合、その損失の一部を控除として申請することもできます。全額ではありませんが、とても助かります。

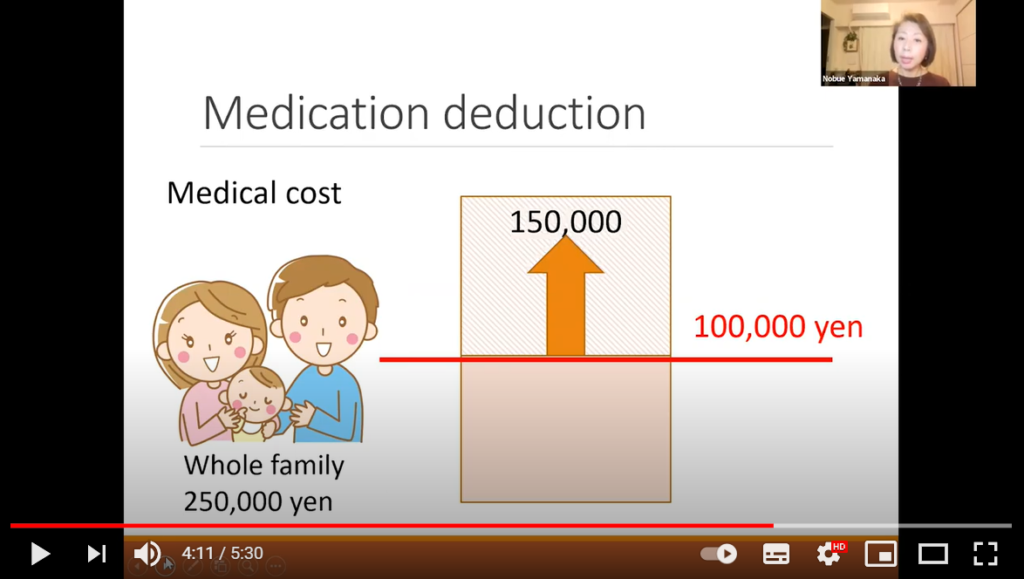

Medication deduction is one of well-known deduction. For example this family spent a medical cost250,000 yen for a year as whole family. He can claim 150,000 yen as a medication deduction. Because the cost of over 100,000 yen is regarded as a medication deduction.

医療費控除はよく知られている控除です。例えば家族として年間の医療費が25万円かかったとします。その場合、世帯主が15万円を医療費控除として申請することができます。なぜならば医療費のうち10万円を超えた分が医療費控除として認められるからです。

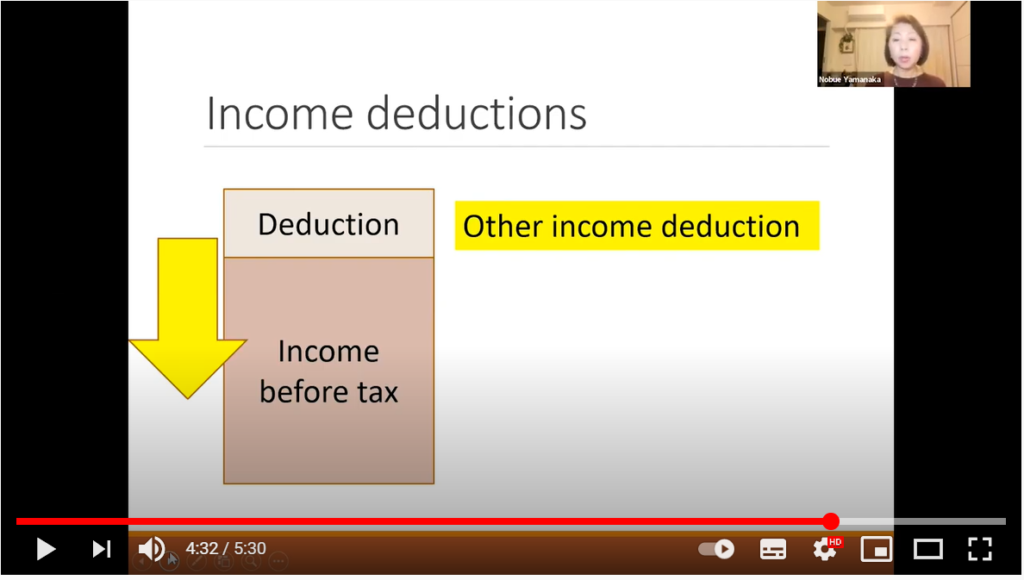

So far I’m talking about income deduction which are deducted from your annual income. As a result your income before tax is decreased, so you can save some money.

これまでのところで所得控除についてお話をしました。所得控除を活用すると結果として課税所得を減らすことになり節税することができます。

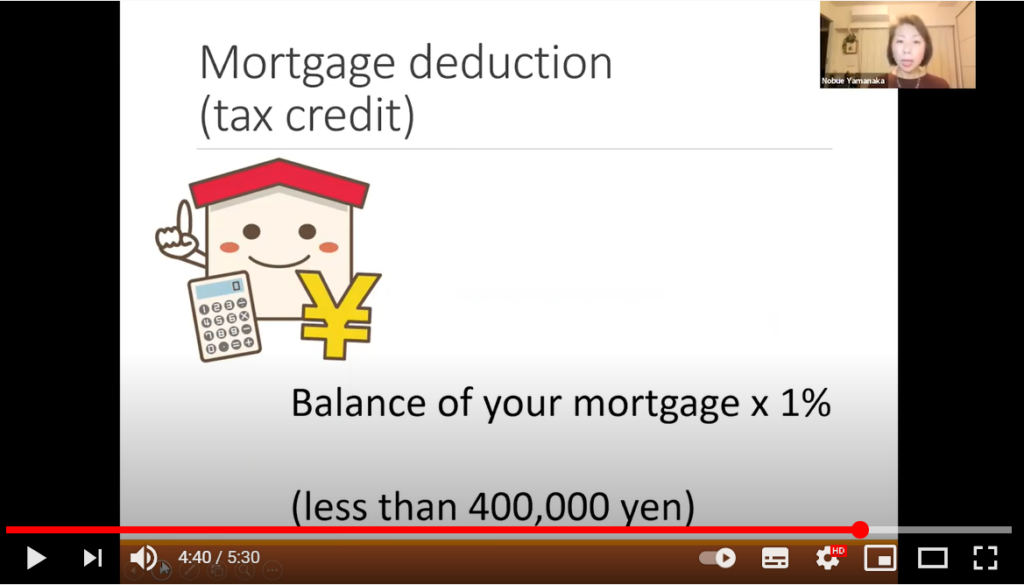

However the last one is little bit different from others. Mortgage deduction is tax credit not income deduction. The amount of the deduction is deducted from your income tax directory. If you have a house loan one percent of your mortgage is deducted as a mortgage deduction.

しかしながら最後の控除はいままでのものと少し違います。住宅ローン控除は、所得控除ではなく税額控除なので、所得税から直接差し引かれます。もし住宅ローンがあればその残高の1%を住宅ローン控除とすることができます。